How do I calculate the covariance between 2 risky assets?

1 Answer

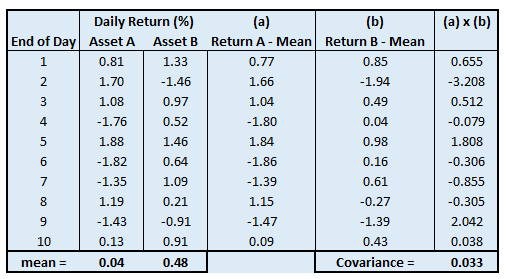

Create a table (Excel?) that displays the daily returns for the two assets over some period of time.

Explanation:

It is easiest to provide an example. The table below shows two assets (A and B). I created random daily returns for each asset.

Here is the formula for Covariance:

Covariance

It looks ominous , but it is actually quite simple. In the table below I calculated the mean (or average) return over 10 days. This mean value is

Next, subtract these mean values from the respective returns for each day (see table below).

Finally, multiply the results from above for each day, add it up and divide by 9 (10 days minus 1). This is the covariance and equals 0.033 for this example.

That's it!

In the example there is a positive covariance , so the two assets tend to move together. When one has a high return, the other tends to have a high return as well. If the result was negative , then the two stocks would tend to have opposite returns; when one had a positive return, the other would have a negative return.

A zero covariance may indicate that the two assets are independent .

Read more: Calculating Covariance For Stocks http://www.investopedia.com/articles/financial-theory/11/calculating-covariance.asp#ixzz3ro4B2qTQ

Follow us: Investopedia on Facebook